Navigating the complexities of credit card debt can feel overwhelming, often leading to a cycle of minimum payments that barely scratch the surface of the principal balance. The stress of mounting interest and the feeling of losing control over one's finances are common experiences for many. However, gaining a clear understanding of your debt landscape and establishing a strategic approach is the first vital step towards financial freedom. This journey begins with organization and foresight, making a Credit Card Payment Plan Template an invaluable tool for anyone serious about tackling their credit card obligations head-on.

A well-structured payment plan provides more than just a list of due dates; it offers a roadmap designed to accelerate debt payoff, minimize interest accrual, and ultimately restore financial stability. It transforms an abstract problem into a concrete, manageable project with clear steps and achievable milestones. By visualizing your debt and tracking your progress, you move from a reactive stance to a proactive one, empowering yourself to make informed decisions about your money.

Implementing such a plan requires a commitment to honesty about your financial situation and a willingness to stick to a budget. It's about identifying where your money is going and redirecting funds strategically to make a more significant impact on your debt. The discipline fostered by following a detailed plan is often the catalyst for broader positive financial habits, extending beyond just credit card debt to overall financial health.

For many, the sheer number of credit cards, varying interest rates, and different due dates can create a paralyzing effect. A systematic approach, facilitated by a dedicated template, simplifies this complexity. It allows you to prioritize, strategize, and execute a plan that is tailored to your unique financial circumstances, moving you closer to a debt-free future one payment at a time.

Why a Credit Card Payment Plan is Essential for Financial Freedom

Credit card debt can be a formidable obstacle to achieving financial peace, but its stronghold can be significantly weakened with a targeted strategy. A dedicated credit card payment plan serves as your personal financial compass, guiding you through the often-treacherous waters of high-interest debt. Its primary benefit lies in providing a clear, actionable pathway out of debt, rather than aimlessly making minimum payments.

One of the most compelling reasons to adopt a structured plan is the potential for significant interest savings. Without a plan, payments are often allocated haphazardly, potentially leaving high-interest debts to fester for longer than necessary. A plan enables you to prioritize which debts to tackle first, based on interest rates or balance size, thereby reducing the total amount of interest paid over time. This targeted approach can save hundreds, if not thousands, of dollars that would otherwise go to creditors.

Beyond the financial savings, a payment plan offers invaluable stress reduction. The constant worry about debt can take a toll on mental and physical health. By creating a definitive plan, you replace anxiety with a sense of control and purpose. Watching your balances decrease according to your plan provides tangible evidence of progress, boosting morale and reinforcing positive financial behaviors. It transforms a source of stress into a solvable problem.

Furthermore, effectively managing and paying down credit card debt can lead to a positive impact on your credit score. A lower credit utilization ratio (the amount of credit you're using compared to your total available credit) and a history of consistent, on-time payments are key factors in building a strong credit profile. As your credit score improves, you gain access to better lending terms for mortgages, car loans, and other financial products, opening doors to future financial opportunities. A Credit Card Payment Plan Template helps you stay on track with these crucial aspects.

Finally, a payment plan fosters greater financial literacy and discipline. The process of creating and sticking to a plan requires you to scrutinize your spending, understand your income, and make intentional choices about your money. This newfound awareness often translates into better budgeting habits, increased savings, and a more robust financial foundation for the long term.

Key Components of an Effective Credit Card Payment Plan Template

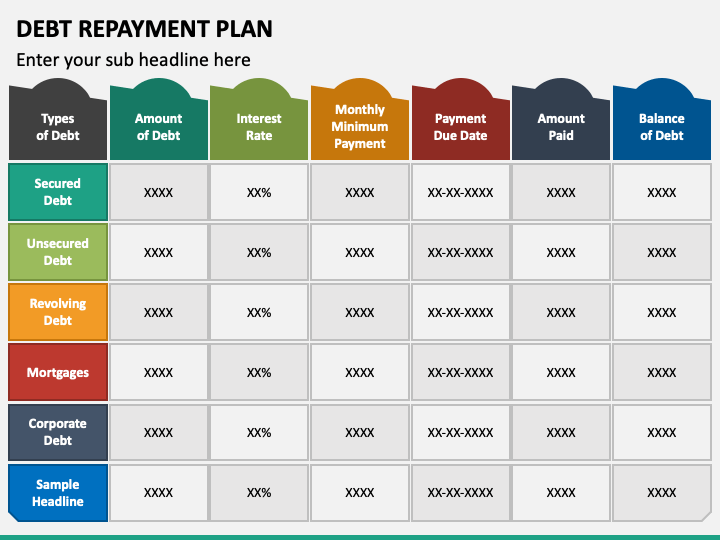

A robust Credit Card Payment Plan Template is more than just a list; it's a dynamic tool that should capture critical information and allow for strategic decision-making. To be truly effective, it must incorporate several key data points and features that empower you to visualize, manage, and conquer your credit card debt.

Comprehensive Card Information

The first step in any template is to list all your credit card accounts. This includes:

* Card Issuer: (e.g., Visa, Mastercard, American Express)

* Card Name: (e.g., Chase Freedom, Discover It)

* Last 4 Digits of Account Number: For easy identification while maintaining security.

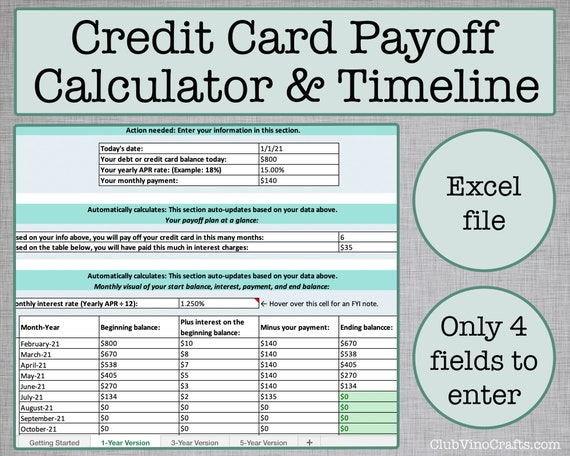

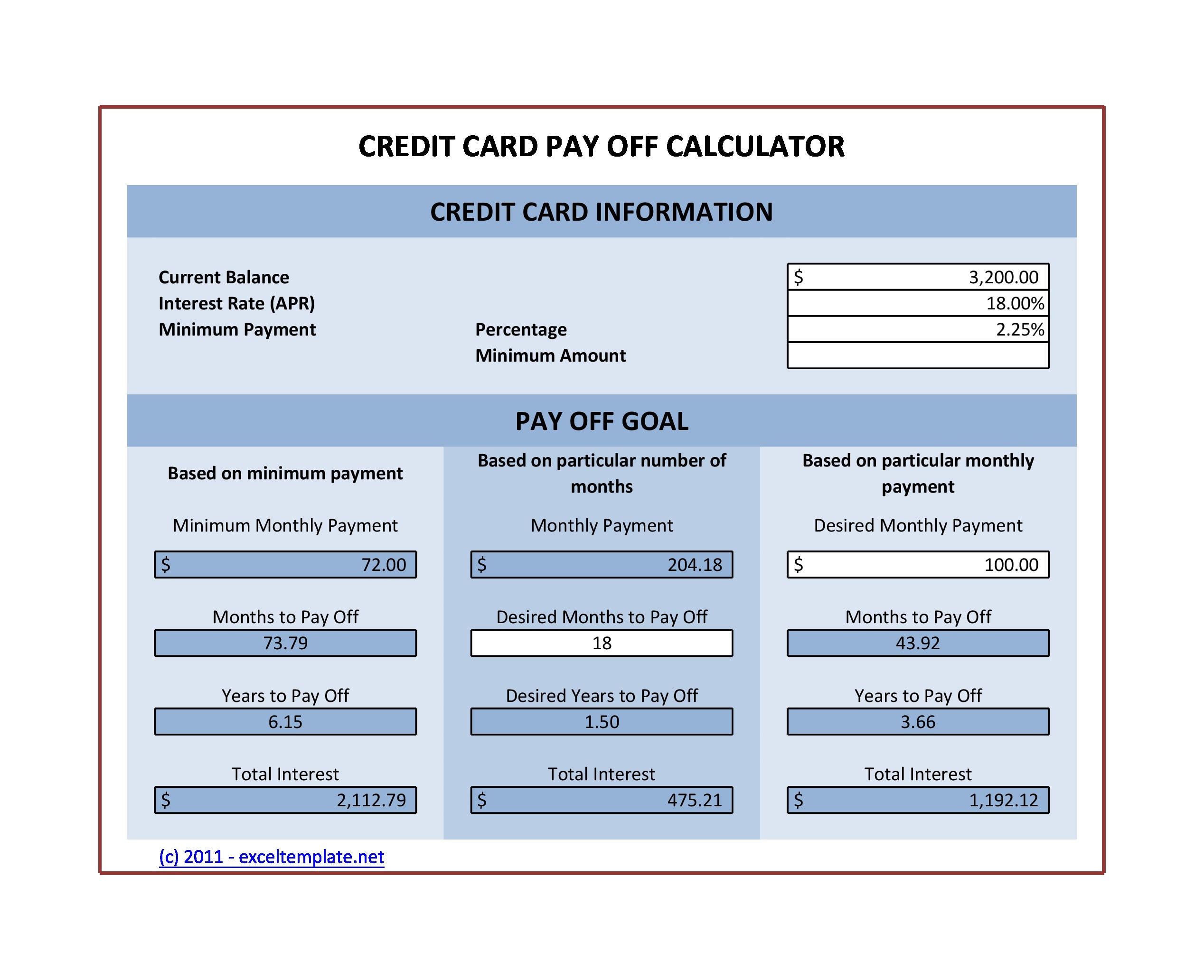

* Current Balance: The precise outstanding amount on each card.

* Interest Rate (APR): Crucial for determining which debts are costing you the most.

* Minimum Payment Due: The smallest amount you must pay each month to avoid late fees.

* Due Date: To ensure timely payments and avoid penalties.

This central repository of information eliminates the need to log into multiple accounts or sift through various statements, providing a clear, consolidated view of your debt landscape.

Debt Reduction Strategy Integration

An effective template isn't just about listing; it's about strategizing. It should allow you to implement a chosen debt reduction method:

* Debt Snowball Method: Prioritizing the smallest balance first for psychological wins.

* Debt Avalanche Method: Prioritizing the highest interest rate first for maximum financial savings.

* Custom Strategy: A blend of both or another method entirely.

The template should have fields to designate which card is the "target" for extra payments each month based on your chosen strategy, and then track the impact of those extra payments on the principal.

Payment Allocation and Tracking

This is where the plan comes to life. Your template should include:

* Total Available for Payments: The total amount you can realistically commit to credit card payments each month, beyond just minimums.

* Minimum Payment Column: Showing the minimum payment made for each card.

* Extra Payment Column: Clearly indicating where any additional funds are being directed.

* Date Paid: To track payment history and ensure accuracy.

* New Balance: After each payment, update the balance to reflect progress.

Regularly updating these fields helps you monitor progress, stay accountable, and adjust your plan as needed.

Projected Payoff Dates and Interest Savings

Advanced templates, or those built in spreadsheets, can automatically calculate projected payoff dates for each card and the total debt, based on your payment strategy. They can also estimate the total interest saved by aggressively paying down debt versus only making minimum payments. These projections serve as powerful motivators, showing you the tangible rewards of your efforts.

Budget Integration (Optional but Recommended)

While not strictly part of the payment plan itself, a truly holistic template might include a small section or link to your overall budget. Understanding your income and expenses is fundamental to determining how much extra you can allocate to debt repayment. This ensures your payment plan is realistic and sustainable within your broader financial picture.

Choosing Your Debt Reduction Strategy for Your Credit Card Payment Plan Template

When creating your Credit Card Payment Plan Template, one of the most crucial decisions you'll make is choosing the debt reduction strategy that best fits your personality and financial situation. Two primary methods stand out: the debt snowball and the debt avalanche. Both are effective, but they appeal to different motivational drivers.

The Debt Snowball Method

The debt snowball method focuses on psychological wins. With this approach, you list all your debts from the smallest balance to the largest, regardless of interest rate. You make minimum payments on all debts except for the one with the smallest balance, to which you direct all your extra available funds. Once the smallest debt is paid off, you take the amount you were paying on that debt (its minimum payment plus the extra funds) and add it to the minimum payment of the next smallest debt. This creates a "snowball" effect, as the amount you're paying towards each subsequent debt grows, accelerating its payoff.

- Pros: Highly motivating as you quickly eliminate smaller debts, providing a sense of accomplishment and momentum.

- Cons: You might pay more interest over time compared to the avalanche method, as it doesn't prioritize high-interest debts.

- Best for: Individuals who need quick wins to stay motivated, or those with many small debts that feel overwhelming.

The Debt Avalanche Method

The debt avalanche method prioritizes financial efficiency. With this strategy, you list all your debts from the highest interest rate to the lowest. Similar to the snowball method, you make minimum payments on all debts except for the one with the highest interest rate, to which you apply all your extra funds. Once the highest-interest debt is paid off, you take the entire payment amount (its minimum payment plus the extra funds) and apply it to the debt with the next highest interest rate. This method consistently targets the most expensive debt first.

- Pros: Saves the most money on interest over the long run, leading to the fastest overall debt payoff from a financial perspective.

- Cons: Can be less motivating in the beginning if your highest-interest debt also has a large balance, as it takes longer to see a debt fully eliminated.

- Best for: Individuals who are driven by numbers and maximizing financial savings, or those with high-interest debts that are eating away at their budget.

Integrating Your Strategy into the Credit Card Payment Plan Template

Regardless of which method you choose, your Credit Card Payment Plan Template should clearly reflect your chosen strategy.

* For Snowball: Your template should list cards ordered by balance (smallest to largest) and highlight which card is the current "target" for extra payments.

* For Avalanche: Your template should list cards ordered by interest rate (highest to lowest) and highlight the current "target" for extra payments.

Ensure your template has dedicated columns for minimum payments and an "extra payment" column, allowing you to easily track how your additional funds are being allocated according to your chosen strategy. Regular review of your template will keep you aligned with your chosen method and ensure you're making consistent progress.

Step-by-Step Guide to Using Your Credit Card Payment Plan Template

Once you have a suitable Credit Card Payment Plan Template, the next step is to populate it and put it into action. This methodical approach will transform your debt from a source of anxiety into a manageable project.

Step 1: Gather All Necessary Information

The first and most critical step is to collect every piece of information related to your credit card debts. This includes:

* Account Statements: Pull up your most recent statements for all credit cards.

* Online Account Access: Log into each credit card account to verify balances, interest rates, and minimum payments.

* Personal Financial Records: Any other documentation that helps you understand your complete debt picture.

Record the following for each card in your template: card name, issuer, last 4 digits, current balance, interest rate (APR), minimum payment, and due date. Don't forget any store cards or lines of credit that function like credit cards.

Step 2: Assess Your Monthly Budget and Available Funds

Before you can make extra payments, you need to know how much extra you can pay.

* Create a Detailed Budget: Track all your income and expenses for at least a month. Categorize spending to identify areas where you can cut back.

* Identify Disposable Income: Determine how much money is left over after all essential expenses (housing, utilities, food, transportation) and current minimum debt payments. This is your "extra payment fund."

* Be Realistic: It's better to start with a smaller, sustainable extra payment than to overcommit and get discouraged.

Your budget is the foundation for a sustainable Credit Card Payment Plan Template. Without knowing your cash flow, your plan will lack accuracy.

Step 3: Choose Your Debt Reduction Strategy

As discussed, decide whether the debt snowball (smallest balance first) or debt avalanche (highest interest rate first) method aligns better with your financial goals and psychological needs. This choice will dictate the order in which you aggressively tackle your debts. Mark this clearly in your template, perhaps by reordering your cards or highlighting your target card.

Step 4: Populate Your Credit Card Payment Plan Template

Enter all the gathered information into your chosen template.

* List Cards: Arrange them according to your chosen strategy (smallest balance first for snowball, highest APR first for avalanche).

* Fill in Details: Carefully input the current balance, APR, minimum payment, and due date for each card.

* Allocate Extra Payments: Decide how much of your "extra payment fund" will go towards your target card. The remaining cards will receive only their minimum payments.

Ensure all figures are accurate. A small error can skew your entire plan.

Step 5: Set Realistic Payoff Goals and Monitor Progress

With your template filled, you can now project your payoff timeline.

* Calculate Projected Payoff Dates: Many templates, especially spreadsheet-based ones, can auto-calculate this. If not, you can manually estimate by seeing how many months it takes to pay off the target debt with your extra payments.

* Schedule Payments: Set up automatic payments for minimums on all non-target cards to avoid missing due dates. Manually schedule the extra payment to your target card.

* Regularly Update and Review: At least once a month, after your payments have posted, update your template with the new balances. This visualization of decreasing debt is a powerful motivator. Review your budget to see if you can free up more funds for extra payments.

* Adjust as Needed: Life happens. If your income changes or unexpected expenses arise, don't abandon the plan. Adjust your extra payment amount in the template and recalculate. The template is a living document designed to adapt.

By diligently following these steps with your Credit Card Payment Plan Template, you'll transform a daunting task into an achievable mission, steadily working your way towards financial freedom.

Beyond the Template: Additional Strategies for Debt Management

While a Credit Card Payment Plan Template is an indispensable tool, it's part of a larger ecosystem of financial strategies designed to eliminate debt and build lasting financial health. To maximize your debt repayment efforts and prevent future accumulation, consider integrating these additional tactics.

Strict Budgeting and Expense Reduction

The foundation of any successful debt reduction plan is a solid budget. Your payment plan dictates how you allocate funds, but your budget ensures those funds are available in the first place.

* Track Everything: Understand exactly where your money goes. Use apps, spreadsheets, or pen and paper.

* Identify Unnecessary Spending: Look for areas to cut back – dining out, subscriptions you don't use, impulse purchases. Every dollar saved can be redirected towards your debt.

* Cash Envelope System: For some, using cash for discretionary spending helps limit overspending.

Reducing expenses directly increases the amount you can allocate to your credit card debt, accelerating your payoff timeline.

Increasing Income

Sometimes, cutting expenses isn't enough, or there's simply no more fat to trim. In such cases, increasing your income can significantly boost your debt repayment efforts.

* Side Hustle: Consider freelancing, gig work, or selling unused items.

* Overtime: If available at your current job, volunteer for extra hours.

* Salary Negotiation: If due for a review, prepare to negotiate for a raise.

Even a modest increase in income, consistently applied to your debt, can make a substantial difference.

Debt Consolidation and Balance Transfers

These strategies can simplify your repayment and potentially save you money on interest, but they require careful consideration.

* Balance Transfer Credit Card: Moving high-interest balances to a new card with a 0% APR promotional period can give you breathing room to pay down debt without accruing new interest. Be mindful of transfer fees and the expiry date of the promotional period.

* Debt Consolidation Loan: A personal loan taken out at a lower interest rate to pay off multiple credit card debts. This consolidates multiple payments into one, often with a fixed interest rate and a clear payoff date.

* Home Equity Loan/Line of Credit (HELOC): If you own a home, you might access lower interest rates, but remember you're using your home as collateral, which carries risk.

Before pursuing these options, assess if the new interest rate and terms truly benefit you, and ensure you won't accumulate new debt on the old cards. These can be powerful tools to support your Credit Card Payment Plan Template.

Negotiating with Creditors

If you're struggling to make payments, don't hesitate to contact your credit card companies. They may be willing to work with you.

* Lower Interest Rates: Ask if they can reduce your APR, even temporarily.

* Payment Plans: Some creditors offer hardship programs that might reduce minimum payments or temporarily suspend payments.

* Settlement: In severe cases, they might agree to accept a lower lump sum than the total owed to close the account, though this can negatively impact your credit score.

Avoiding New Debt

Perhaps the most crucial long-term strategy is to avoid accumulating new debt while paying off old debt.

* Cut Up Cards (or Freeze Them): If impulse spending is an issue, physically removing access to credit can be effective.

* Emergency Fund: Build a small emergency fund (e.g., $1,000) before aggressively paying off debt, so unexpected expenses don't force you back to using credit.

* Mindful Spending: Before every purchase, ask yourself if it's a need or a want, and if it aligns with your financial goals.

By combining the organizational power of a Credit Card Payment Plan Template with these broader debt management strategies, you create a holistic approach that not only eliminates current debt but also fosters enduring financial stability.

Customizing Your Credit Card Payment Plan Template

A generic Credit Card Payment Plan Template provides a solid starting point, but true effectiveness comes from tailoring it to your unique financial situation and personal preferences. Customization ensures the plan is realistic, motivating, and sustainable for you.

Adapting to Your Financial Reality

Your template should reflect your actual income, expenses, and debt load.

* Flexible Payment Amounts: Don't stick rigidly to a pre-set "extra payment" amount if your income fluctuates. Build in flexibility to adjust your additional contributions month-to-month. On months with bonuses or fewer expenses, you might contribute more; on tighter months, you might stick to just minimums. Your template should allow for easy modification of these figures.

* Emergency Fund Integration: Some people prefer to build a small emergency fund before tackling debt aggressively. Others integrate a small contribution to savings alongside debt payments. Your template can include a line item to track this dual goal, reminding you to fund both.

* Irregular Income: If your income is variable (e.g., freelance, commissions), your template might include a section to project or track average income, allowing you to set a conservative, yet achievable, base amount for debt payments.

Personalizing for Motivation and Clarity

The design and layout of your template can significantly impact your engagement.

* Visual Cues: Incorporate progress bars, color-coding, or graphs to visually track your debt reduction. Seeing a bar fill up or a balance turn green can be incredibly motivating.

* Goal Setting Section: Include a dedicated space for your "why." Why are you paying off this debt? (e.g., "To save for a down payment," "To reduce stress," "To be financially independent"). Referencing this can re-ignite motivation during challenging times.

* Milestone Tracking: Break down your overall debt into smaller, more achievable milestones. For example, "First $1,000 paid," or "Card X paid off." Celebrate these small victories within your template.

* Notes Section: A free-form area to jot down insights, challenges, or thoughts. This can be useful for reflecting on your journey and adapting your strategy.

Choosing the Right Format

The "template" itself can take many forms, and choosing the right one for you is a crucial customization step.

* Spreadsheets (Excel, Google Sheets): Offer maximum flexibility for calculations, automation, and visual tracking. You can create custom formulas for projected payoff dates and interest savings. Many free templates are available online that you can then modify.

* Printable PDF Templates: Great for those who prefer a tangible, pen-and-paper approach. Look for templates with clear sections and ample space for writing.

* Budgeting Apps with Debt Management Features: Some personal finance apps (e.g., YNAB, Mint, Personal Capital) have built-in debt management tools that can act as a dynamic template, often linking directly to your accounts for real-time updates.

* Simple Notebook: For a truly minimalist approach, a well-organized notebook can serve as your template, though it requires manual calculations.

The best Credit Card Payment Plan Template is the one you will consistently use and update. Don't be afraid to experiment with different formats and elements until you find what resonates most with your personal style and financial goals. A customized template becomes a powerful partner in your journey to debt freedom.

Conclusion

Tackling credit card debt can feel like an uphill battle, but with the right tools and strategies, it's an entirely achievable goal. The Credit Card Payment Plan Template emerges as a foundational element in this endeavor, offering a structured, clear, and actionable roadmap to financial freedom. By consolidating all crucial debt information, enabling the strategic allocation of payments, and providing a means to track progress, it transforms an abstract problem into a manageable project.

We've explored why such a plan is indispensable, delving into its power to save on interest, reduce stress, and improve your credit score. We've broken down the key components that make a template effective, from comprehensive card details to strategic payment allocation and projected payoff dates. The choice between the debt snowball and debt avalanche methods allows for personalized motivation, ensuring your plan aligns with your temperament, whether you seek quick wins or maximum financial efficiency.

Furthermore, a step-by-step guide has demonstrated how to effectively use your template, from gathering information and assessing your budget to setting realistic goals and monitoring your journey. Critically, we looked beyond the template itself, highlighting additional strategies such as rigorous budgeting, income generation, debt consolidation, and diligent avoidance of new debt, all of which complement and reinforce your payment plan. Finally, we emphasized the importance of customizing your template to fit your unique financial situation and motivational style, ensuring it remains a living, breathing document that evolves with your progress.

Ultimately, a Credit Card Payment Plan Template is more than just a document; it's a commitment to your financial well-being. By embracing its structure and consistently applying its principles, you empower yourself to systematically dismantle your credit card debt, paving the way for a more secure, less stressful, and truly debt-free financial future.

0 Response to "Credit Card Payment Plan Template"

Posting Komentar